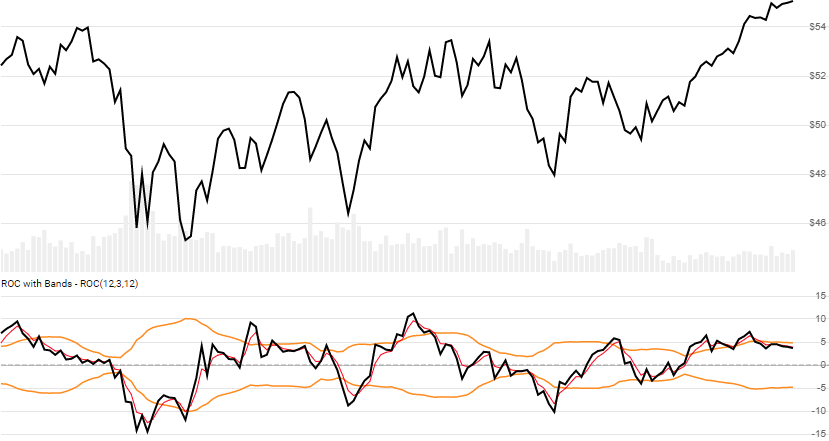

ROC with Bands

Rate of Change (ROC) with Bands, created by Vitali Apirine, is a volatility banded variant of Rate of Change (ROC). [Discuss] 💬

// C# usage syntax

IEnumerable<RocWbResult> results =

quotes.GetRocWb(lookbackPeriods, emaPeriods, stdDevPeriods);

Parameters

lookbackPeriods int - Number of periods (N) to go back. Must be greater than 0. Typical values range from 10-20.

emaPeriods int - Number of periods for the ROC EMA line. Must be greater than 0. Standard is 3.

stdDevPeriods int - Number of periods the standard deviation for upper/lower band lines. Must be greater than 0 and not more than lookbackPeriods. Standard is to use same value as lookbackPeriods.

Historical quotes requirements

You must have at least N+1 periods of quotes to cover the warmup periods.

quotes is a collection of generic TQuote historical price quotes. It should have a consistent frequency (day, hour, minute, etc). See the Guide for more information.

Response

IEnumerable<RocWbResult>

- This method returns a time series of all available indicator values for the

quotesprovided. - It always returns the same number of elements as there are in the historical quotes.

- It does not return a single incremental indicator value.

- The first

Nperiods will havenullvalues for ROC since there’s not enough data to calculate.

RocWbResult

Date DateTime - Date from evaluated TQuote

Roc double - Rate of Change over N lookback periods (%, not decimal)

RocEma double - Exponential moving average (EMA) of Roc

UpperBand double - Upper band of ROC (overbought indicator)

LowerBand double - Lower band of ROC (oversold indicator)

Utilities

See Utilities and helpers for more information.

Chaining

This indicator may be generated from any chain-enabled indicator or method.

// example

var results = quotes

.Use(CandlePart.HL2)

.GetRocWb(..);

Results can be further processed on Roc with additional chain-enabled indicators.

// example

var results = quotes

.GetRocWb(..)

.GetEma(..);